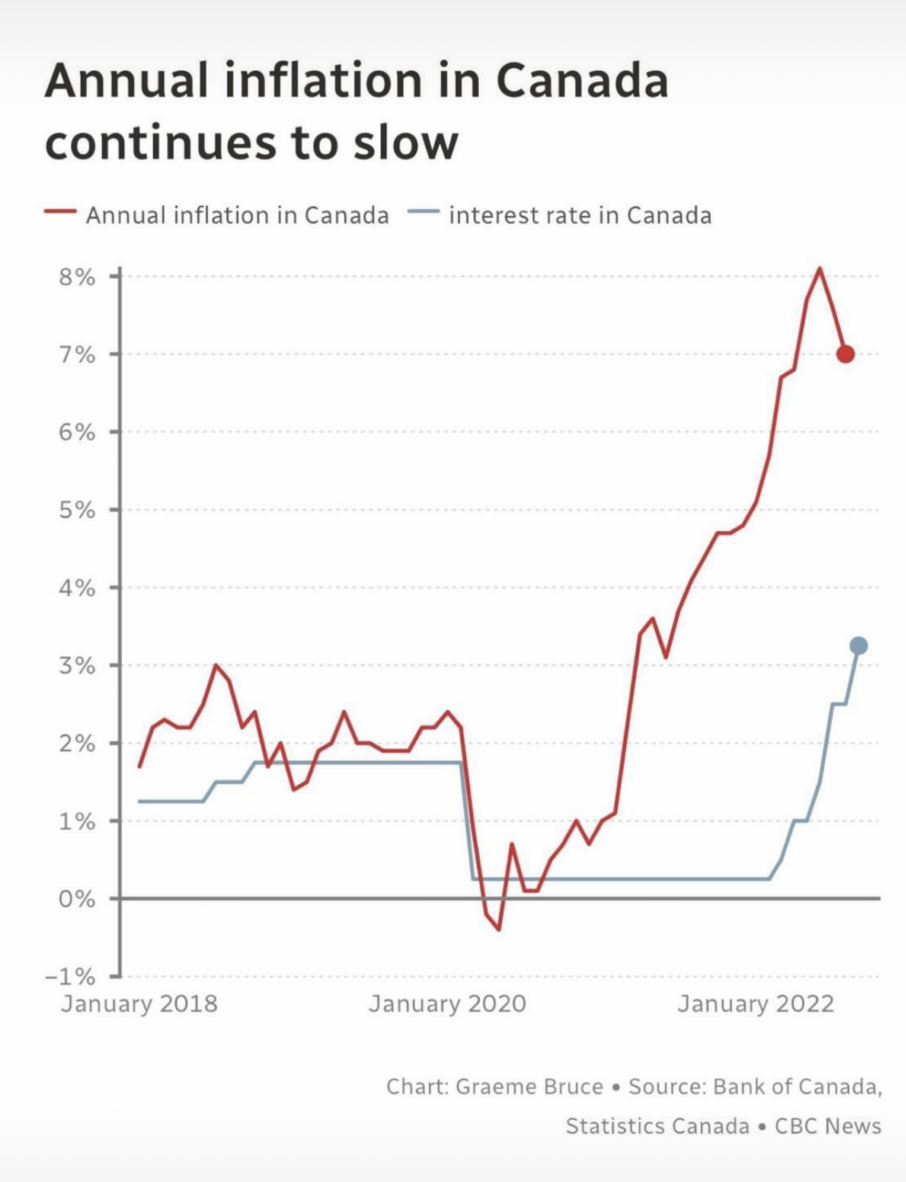

We’re writing this in early November of 2022, just a few weeks after the latest government announcement to raise the prime rate by an additional +0.5%.

This brings the total 2022 policy interest rate increases up to +3.5%, with one more announcement before the end of the year scheduled for December 7th.

While it looks like the worst is over, it has still been pretty painful.

Unfortunately, the best “medicine” to cure rising inflation is to raise interest rates

Until we reach a target rate of 2% inflation, don’t expect the Bank of Canada to reverse their position.

They don’t care about raining on the real estate parade.

They don’t care if you default on your mortgage payments.

They don’t care about the overall impact on businesses and the economy.

They WILL get to a 2% rate of inflation, and nothing will stop them. The question we want to answer here is, “What’s so important about that?”

If you bought something for $1 today with a 2% inflation rate, it would take approximately 36 years for it to double in price to $2.

With a 4% rate of inflation, it will take 18 years.

At our current rate of 7-8% inflation, it will take less than 10 years for that coffee to double in price.

This is really a compounding issue. The same compounding that makes your investments grow over your lifetime works against us in an inflationary market.

In other words, the money you earn and save will be worth less and less due to inflation. If you have $10,000 of savings and inflation is at 7%… if things remained the same, your money would only be worth $5,000 in ten years.

That’s a recipe for disaster.

Much scarier than any costume you saw on Hallowe’en!

Since June, we’ve seen the “headline” rate of inflation trending down from 8.1% to 6.9%.

It’s not where we want or need it to be, but it’s headed in the right direction.

Many economists think the Bank of Canada has already overshot the mark and have triggered a technical recession. In fact, every recession in history has been triggered by central banks being overzealous in their rate hikes.

Only time will tell, because inflation metrics are a lagging indicator that tells us what happened months ago.

In the meantime, expect the rate hikes to slow down or stop at some point soon, and we’ll see current rates stay static for most of 2023, then a likely decline to get us to “neutral”.

How much decline? Hard to say, but the goal is to get back to “neutral”.

In other words, the goal is to reach a point where the rate neither stimulates nor restricts the economy. It’s a very delicate balancing act, and we’ll be watching it closely.