For years, we enjoyed a very low interest rate environment. But in 2017, things changed and we began seeing interest rates rise. At the time of writing this, we’ve experienced four interest rate increases, and there are likely more to come.

Plus, we’ve seen two stress-tests implemented in 2016 and 2018 that artificially “raised” the standard of qualification for buyers. Even though their ACTUAL interest rate is lower, buyers must now qualify at an interest rate roughly 2% higher with the stress-test. Practically speaking, this reduced the maximum purchase price for most buyers by about 16-17%.

When we speak about mortgages to most clients, their eyes just glaze over. This post is an attempt at making things easy to understand. Let’s start by looking at what’s likely to happen when rates DO go up, and then we’ll look at what determines interest rates.

What happens to affordability when interest rates go up?

A sample $100,000 income earner today can qualify for a $540,000 mortgage (we’re rounding numbers for the example). This is based on a standard 25-year mortgage, with interest rate around the mid-3% range.

If the rate goes up by 1/4%, that number will drop by 2.4% to $527,000.

If the rate goes up 1/4% again, another 2.4% drop, and so forth.

If we are to expect a 1% increase in rates by the end of 2019 (as some are expecting), that’ll mean this sample $100K/year income buyer will qualify for 9.6% less mortgage.

TAKEAWAY: For each 1% increase in interest rates, you’re able to buy approximately 10% less property.

In a market that is not expected to have major price gains, but is not expected to drop, that 9.6% can mean the difference between getting in or staying out.

We’re not here to push anybody to buy a property that they can’t afford. But if you, or someone you know, is considering buying a property, it’s very likely they will be able to buy LESS home next year compared to this year.

That might mean that buyers will need to either move further away to open up their options, or it might mean they’re buying a smaller home with less features.

We are absolutely predicting that people will look back on 2018 and think, “We SHOULD have bought last year” at this time next year in 2019

How do we know this is likely to happen? Well, four interest rate increased and two stress tests… and prices are still creeping up slowly. With a loss of more than 25% of purchasing power, you would think that prices would have come down. But that hasn’t happened.

That means the demand to buy housing in southern Ontario right now is extremely strong, and it doesn’t appear to be changing. With land-use policies still restrictive, and the cost to move remaining high, the supply doesn’t appear to be increasing either.

BONUS: How are interest rates determined?

In Canada, interest rates are determined by a lot of factors – the policy of the Bank of Canada, the demand for loans, the supply of available lending capital, interest rates in the United States and Europe, inflation rates and other economic factors.

But the easiest way to think about interest rates is to imagine the bank as a middle-man.

When a bank offers you an interest rate on a loan (mortgage), they’re being guided by the rate they get themselves. This market rate is what they’re paying to borrow money for you. They pay a small amount of interest on THEIR loan, so that they can lend to YOU for a higher rate to make profit.

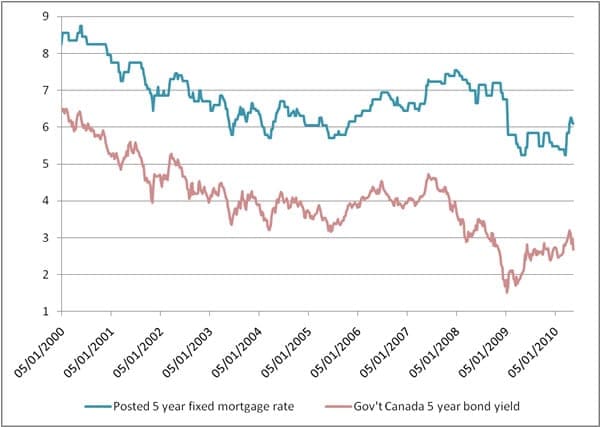

They call this a “spread”, and if it costs more for the bank to borrow money, it will cost YOU more to borrow from the bank. Things have been a little wonky lately, but look at this graph that shows the relationship between 5-year fixed mortgage rates and 5-year bond yields from 2000-2010:

If you’re wondering if interest rates are likely to increase in the short-term, speak to your friendly neighbourhood bond trader!

Interest rates for both long-term and short-term loans are determined by the Bank of Canada, mostly in response to inflation. There are many ways they can look at inflation, but one of them is the Consumer Price Index (CPI), which measures the cost of everyday products for consumers.

If inflation is going up too quickly, the Bank steps in and raises interest rates, using them very much like a brake pedal with a fast-moving car.

TAKEAWAY: Generally speaking, if interest rates are rising, it’s because the economy is improving.

It’s a complicated game, because when you change one thing, it affects everything else. For example, raising interest rates will raise the bond rates, which means we’re paying more interest on our debt, which takes more out of tax revenue from consumers lowering their spending. The end result is a decreased economy, and rates will need to go down accordingly. You get the picture… and this is why our market experiences cycles over and over again.

Knowing is half the battle…

So now you’re equipped with the knowledge and awareness to predict the future, right? 🙂

Unlike the stock market, the housing market is much less volatile, and a little bit more predictable. Provided no major government intervention is on the horizon, we can make predictions based on the economy, the interest rates, and the supply and demand of housing options, which we discuss weekly in the Milton SoldWatch report.

But please remember that you buy housing for the long-term. Nobody we have EVER met regrets buying real estate 25 years later. And it’s not going to get any easier anytime soon. Our best advice is to get your foot in the door any way you can.

Semone did a GREAT podcast about just getting in as soon as you can. Enjoy!