The real estate market in Milton, Ontario, and the Greater Toronto Area (GTA) has faced a whirlwind of changes over the past few years. From inflationary pressures to evolving mortgage rules, homebuyers and sellers have had to navigate a complex landscape over the last few years.

As we step into 2025, optimism is building.

Stabilizing interest rates, robust immigration, and new housing policies are shaping what looks to be a more predictable and positive year for the local housing market.

This article dives into the key factors driving market conditions in 2025.

We’ll explore how inflation, GDP growth, interest rates, and other crucial elements are influencing real estate trends. Whether you’re a first-time buyer, an investor, or simply keeping tabs on the market, this guide provides valuable insights into what to expect in Milton, the GTA, and beyond for the upcoming year.

Inflation & the Consumer Price Index (CPI)

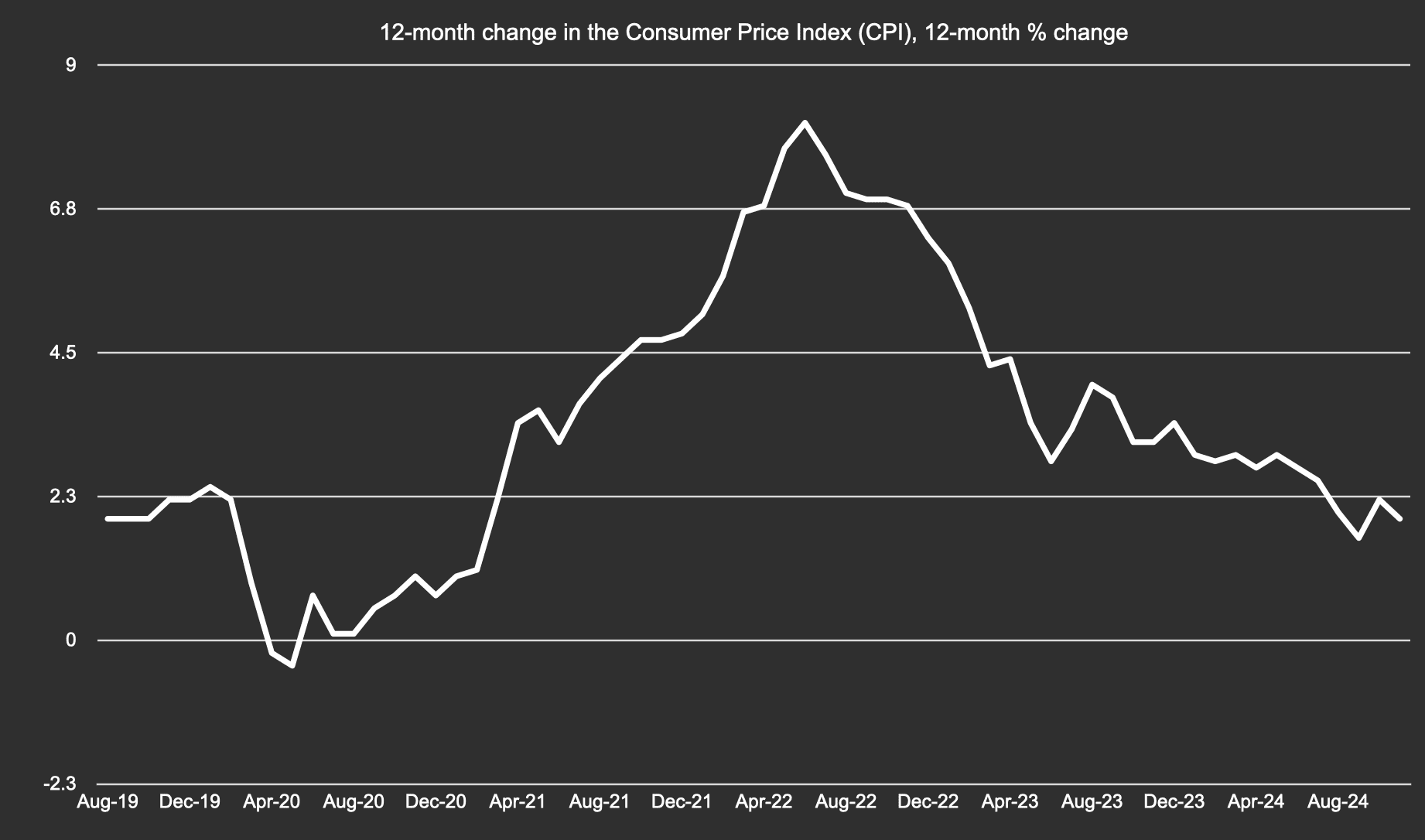

Inflation was a non-issue for many years — until around 2021.

During the pandemic, everything seemed to come to a halt. Supply chain interruptions and increased spending, among other factors, caused price increases and inflation to peak at 8.3%.

High inflation destabilizes economies, eroding savings and straining households.

Recognizing the serious threat, the Bank of Canada took swift action to cool the economy.

As a result, inflation now hovers near the 2% target as we head into 2025.

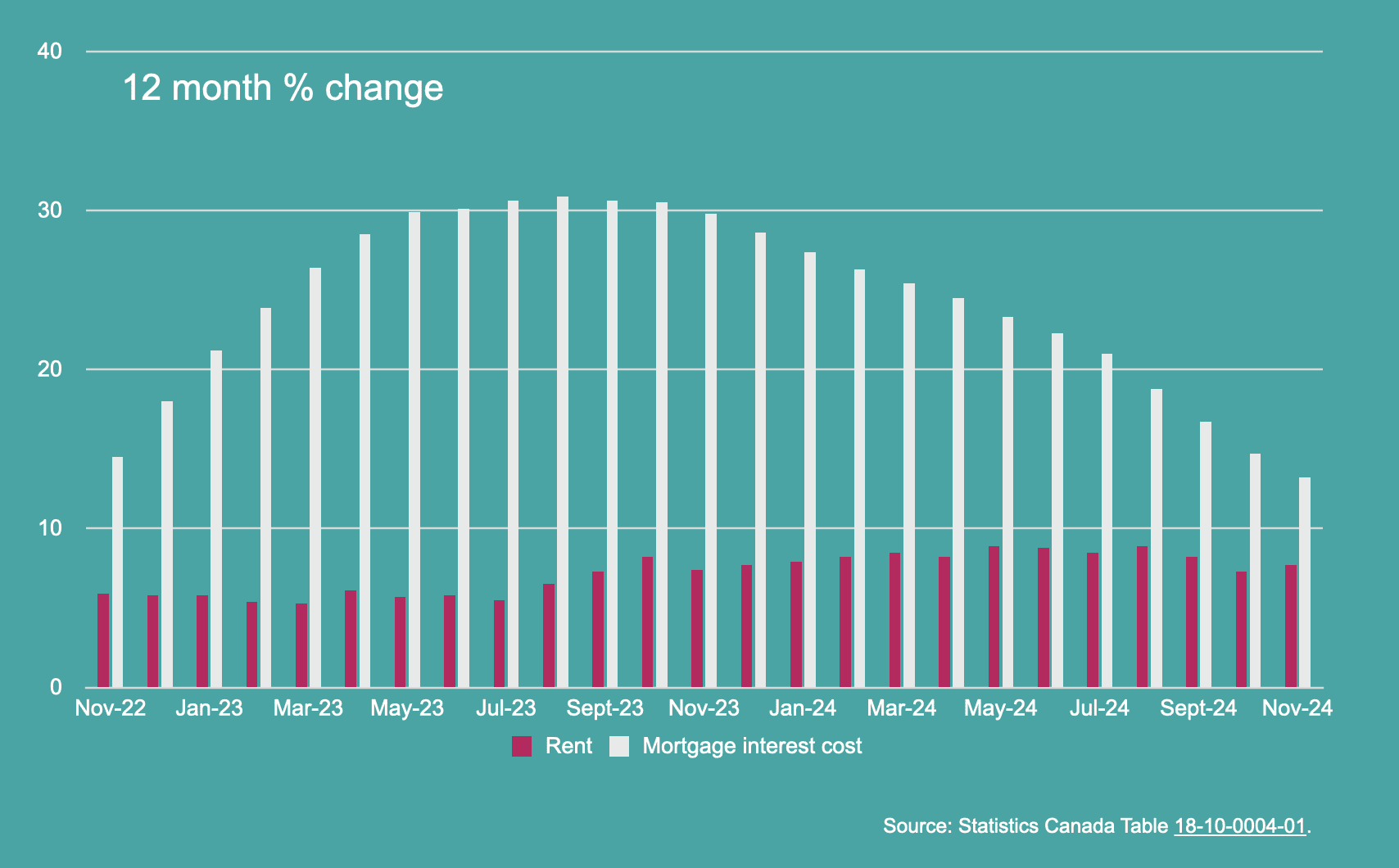

As we compare the cost of renting and borrowing, we’ve seen that upward pressure remains on rents, but mortgage carrying costs have decreased for 15 consecutive months.

This easing of costs has spurred renewed interest from first-time buyers, particularly after the Bank of Canada’s first 50 basis point cut in October 2024.

As rates declined and prices stabilized, a “wait and see” approach shifted to active buyer engagement.

This trend is expected to gain momentum in 2025. Buyers know the time is limited before the pendulum swings back into a market that favours sellers… with likely increased multiple offers and demand.

Gross Domestic Product (GDP) & Labour

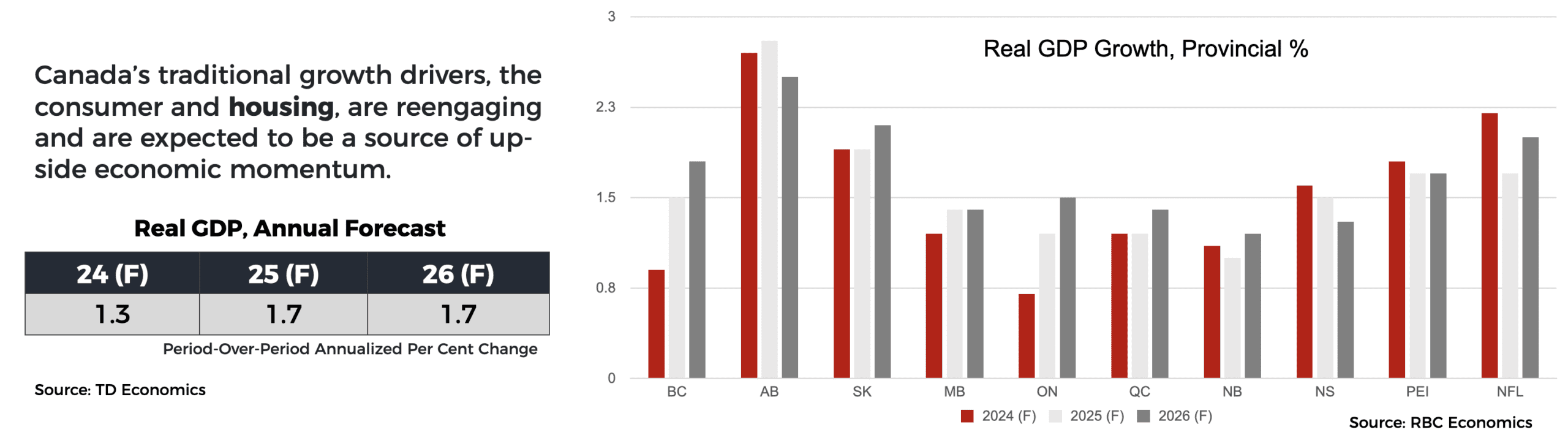

The Canadian economy’s resilience has positioned it for growth in 2025, with housing playing a key role.

TD Economics anticipates that real estate activity will contribute to an upswing in GDP levels.

Ontario’s economy, in particular, is forecasted to strengthen, buoyed by housing demand and economic recovery efforts. RBC Economics predicts steady improvement in the province’s production metrics.

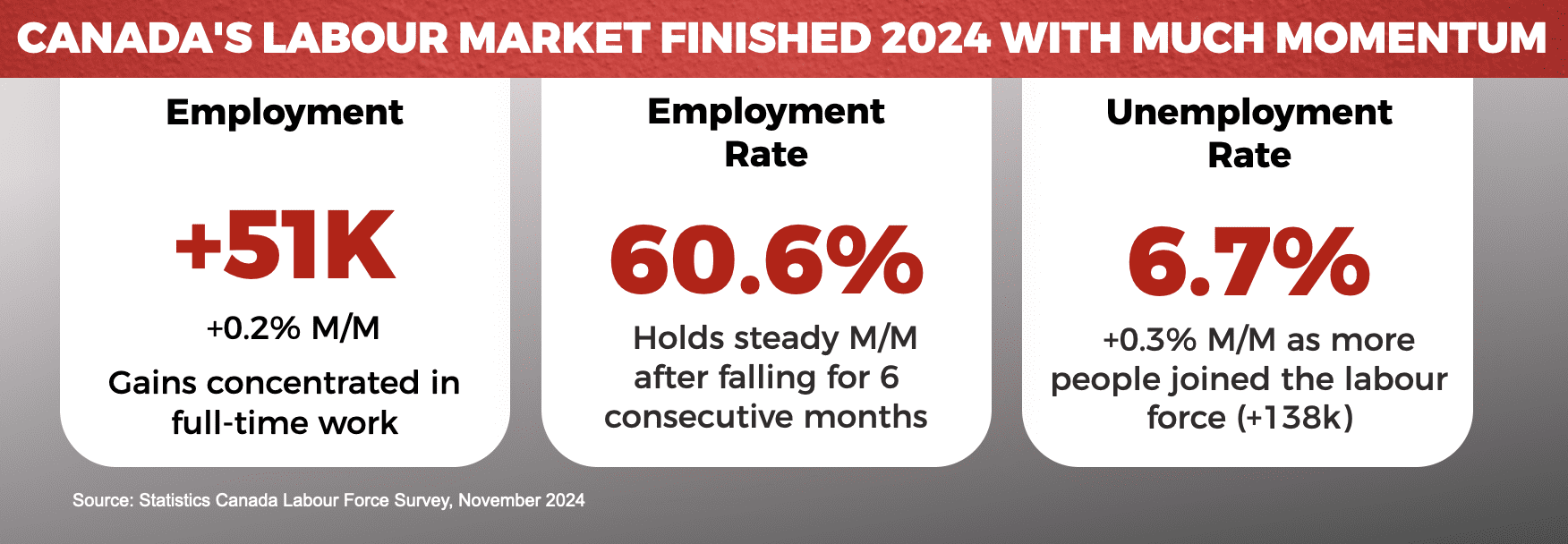

Canada’s labour market finished 2024 with strong employment rates, nearing the 5% unemployment benchmark considered “full employment.”

As interest rates drop, businesses can also better manage costs and invest in labour. This increased employment fuels real estate activity, as more Canadians secure stable, full-time jobs that support homeownership.

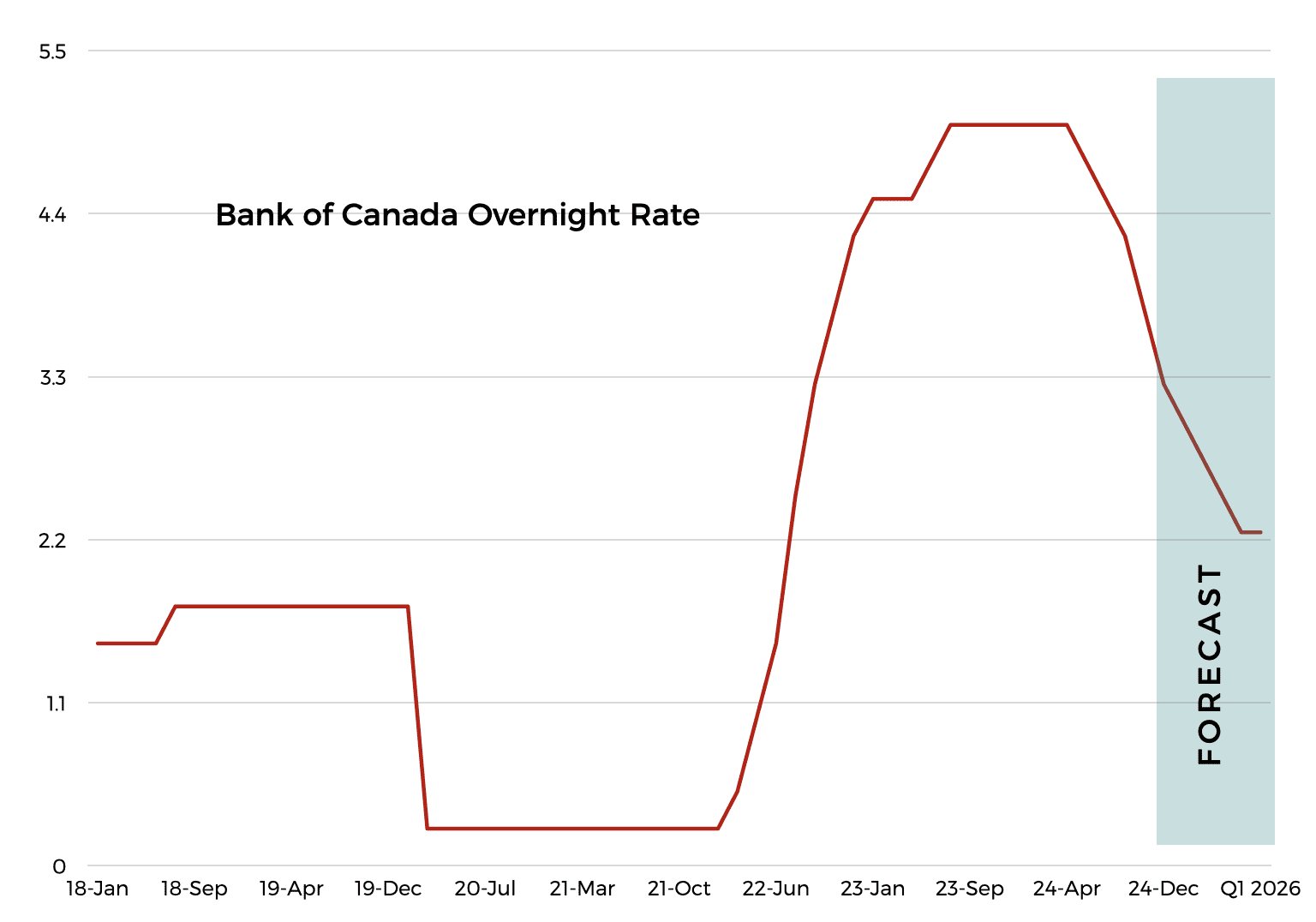

Interest rates & savings

In the latter half of 2024, the Bank of Canada aggressively cut its overnight lending rate by 175 basis points.

With another 100 basis point reduction expected by the end of 2025, borrowing costs are projected to remain favourable.

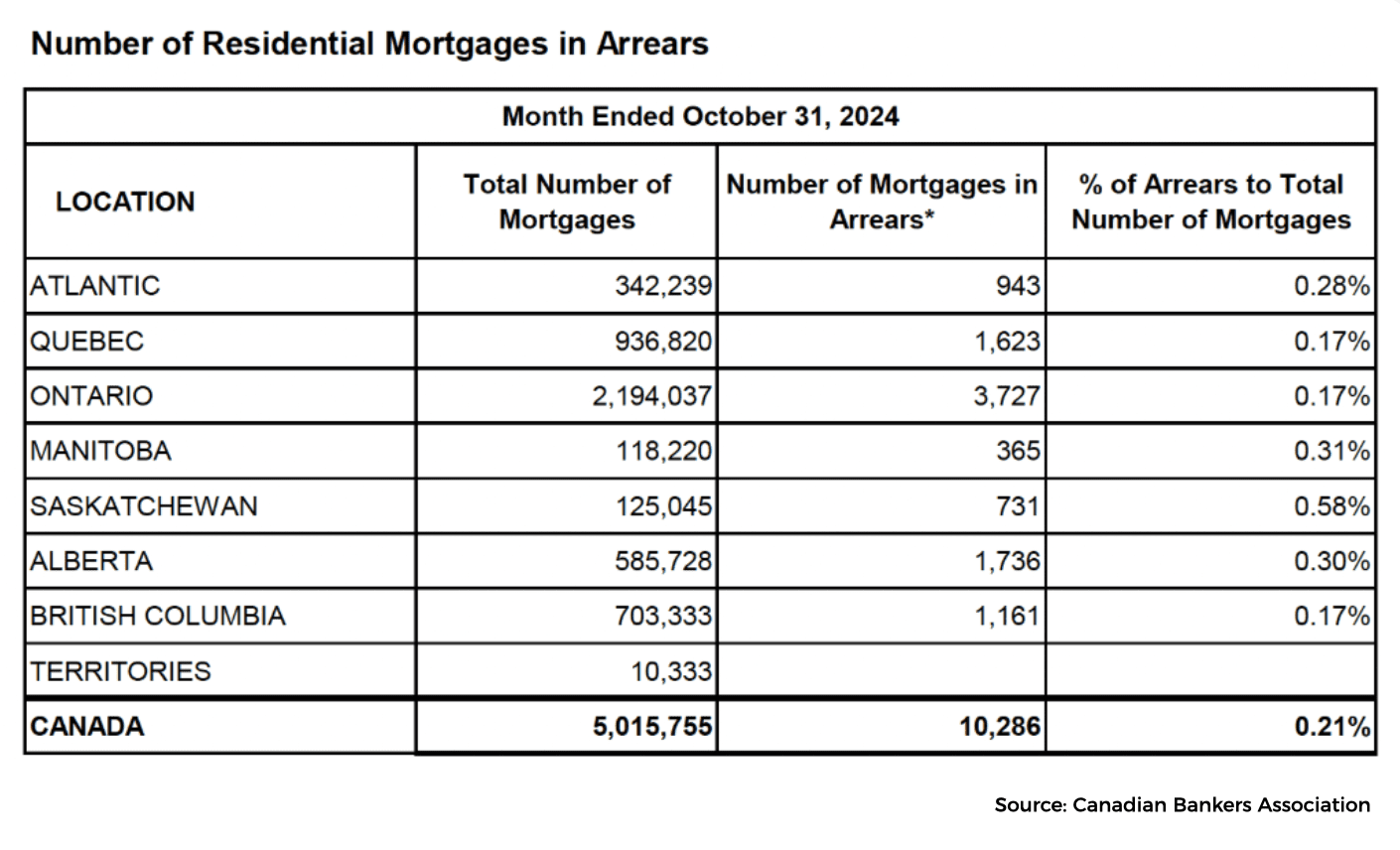

Canada’s mortgage default rate of 0.21% highlights the country’s strong credit health, especially when compared to the United States’ delinquency rate of 3.92%.

Americans are nearly 20 times more likely to be in default of mortgage payments compared to Canadians! (This is also why their housing market always takes longer to recover after a dip)

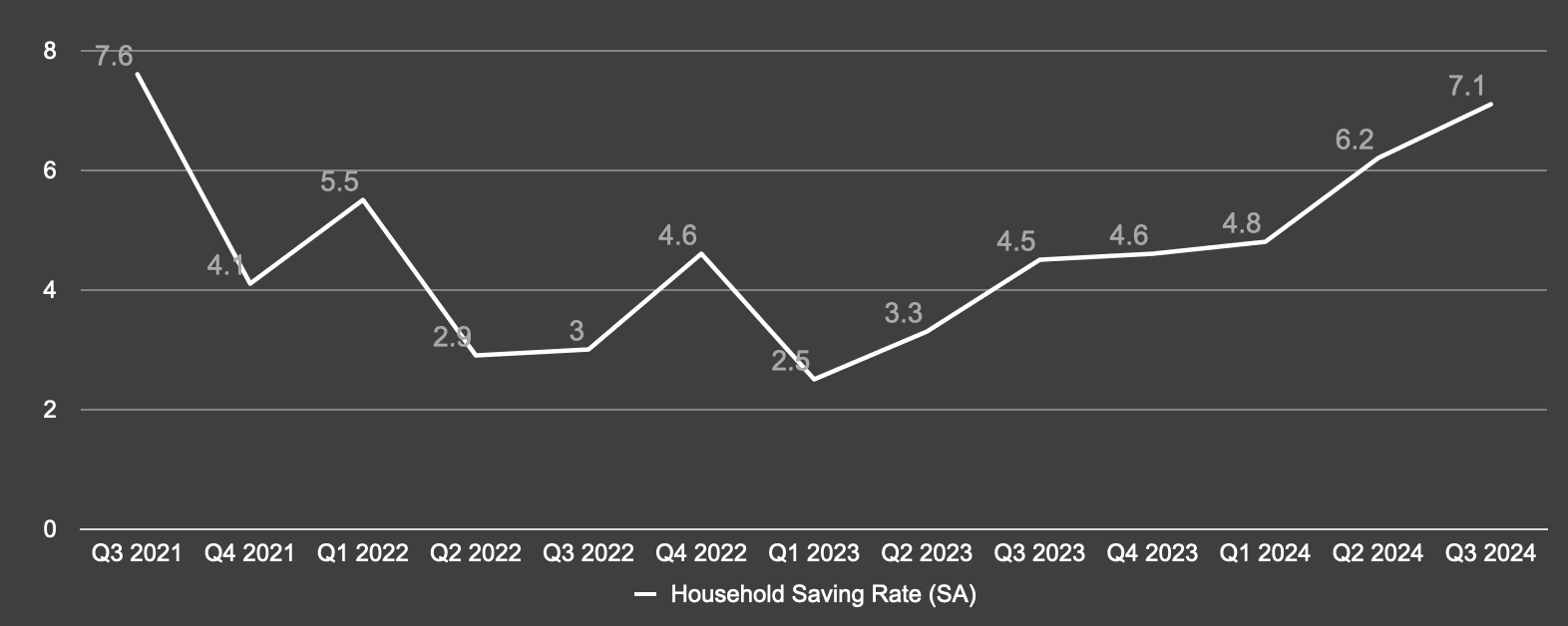

Meanwhile, Canadians have been steadily increasing their savings since 2023.

This trend, coupled with an estimated trillion-dollar wealth transfer from Baby Boomers to younger generations, further boosts financial stability and purchasing power.

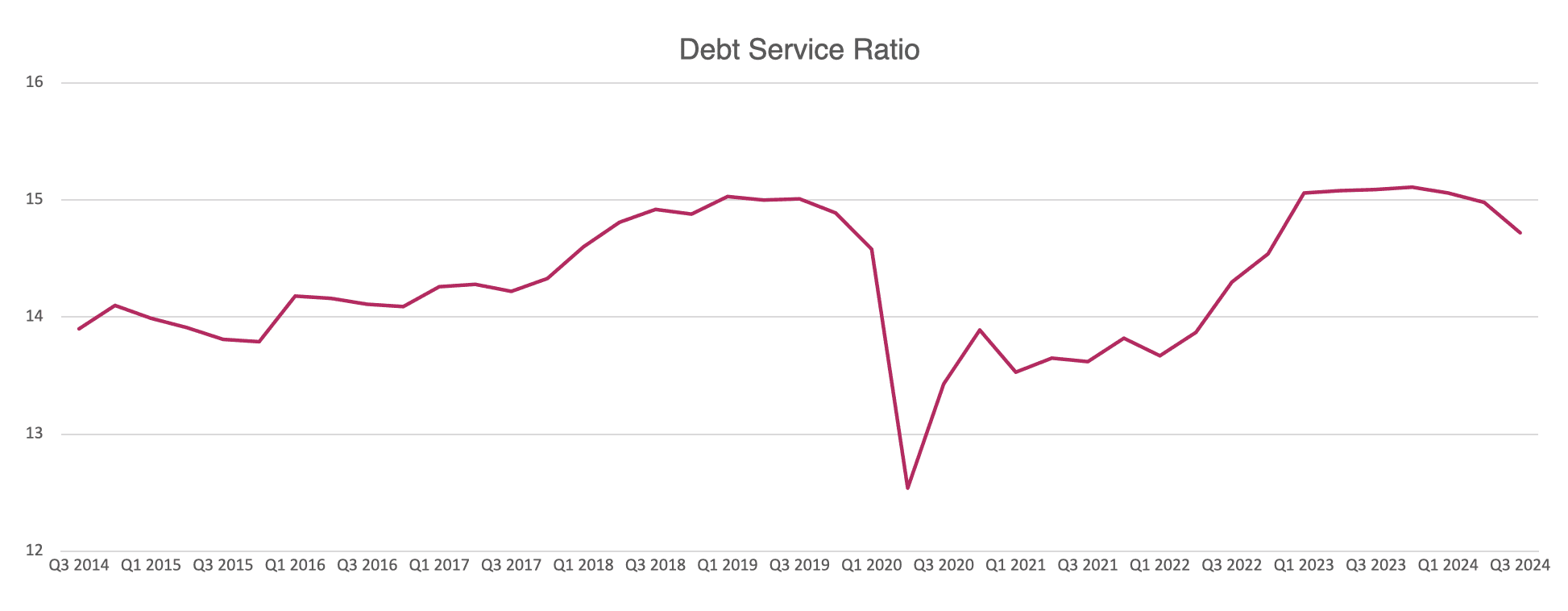

The Debt Service Ratio—which measures household debt relative to income—has also improved.

While inflation briefly strained affordability, the recent drop in debt levels means many Canadians are entering 2025 feeling more financially secure… with a mix of higher salaries and lower debt as a whole.

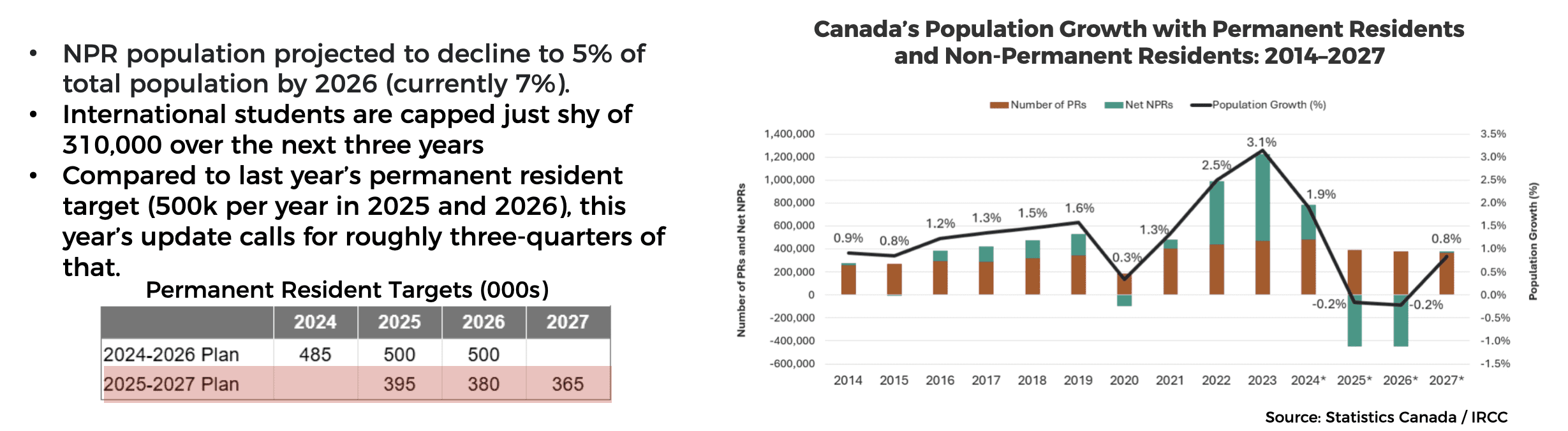

Population growth & immigration

For many years, Canada welcomed 200,000 to 250,000 immigrants annually. Recent years have seen this figure more than double, surpassing 500,000 people per year.

While these numbers are now projected to stabilize at 350,000 to 400,000 annually, the influx has strained a housing market already grappling with supply shortages.

For Milton and the GTA, population growth underscores the critical need for more housing. New residents contribute to economic activity and support social programs, but housing availability remains a pressing concern.

However, with the Foreign Buyer Ban still in place, market activity is largely driven by domestic demand, ensuring that housing remains a local matter.

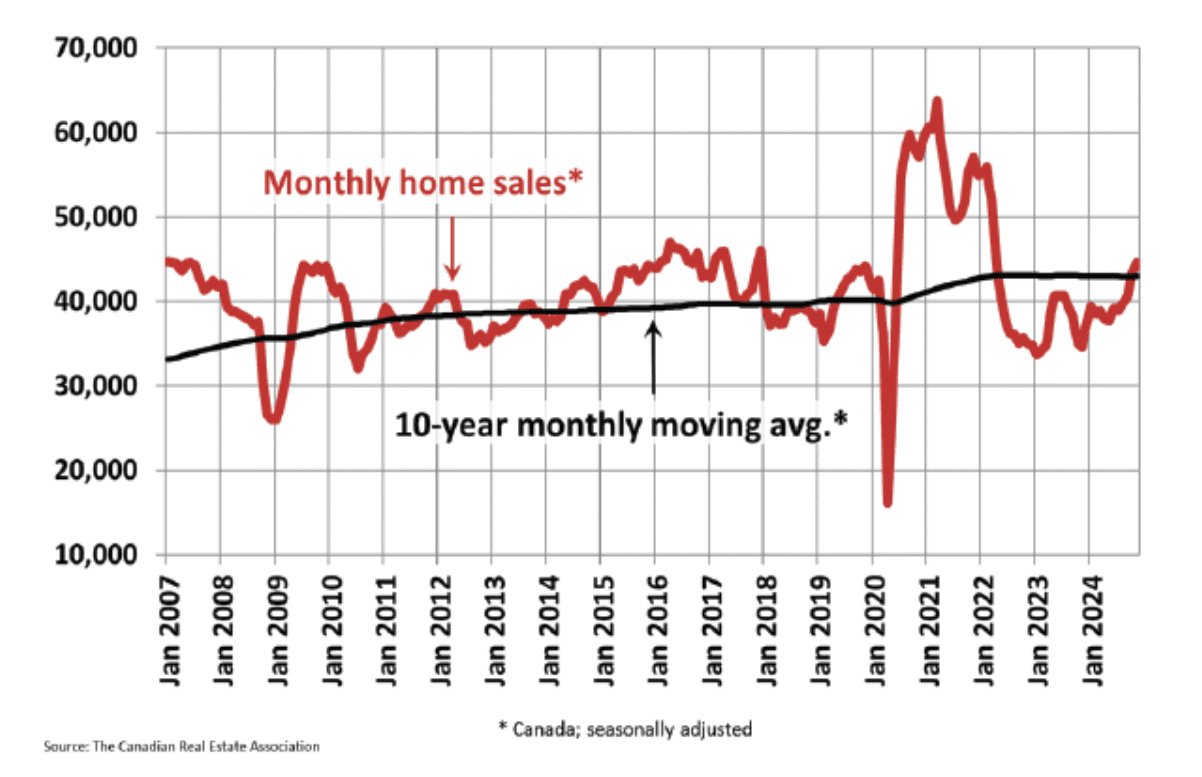

Home sales & demand

The tail end of 2024 showed clear signs of increased housing demand. November sales were up 2.8% month-over-month… and 18.4% higher than May 2024, just before the Bank of Canada’s first rate cut in June.

Notably, monthly sales surpassed the 10-year average for the first time since the early 2022 market peak.

In Milton, real estate transaction volumes rose by over 40% year-over-year in October and November 2024.

Lower borrowing costs and growing buyer confidence contributed to this resurgence. This upward trajectory is expected to continue into 2025 as more buyers take advantage of improved affordability.

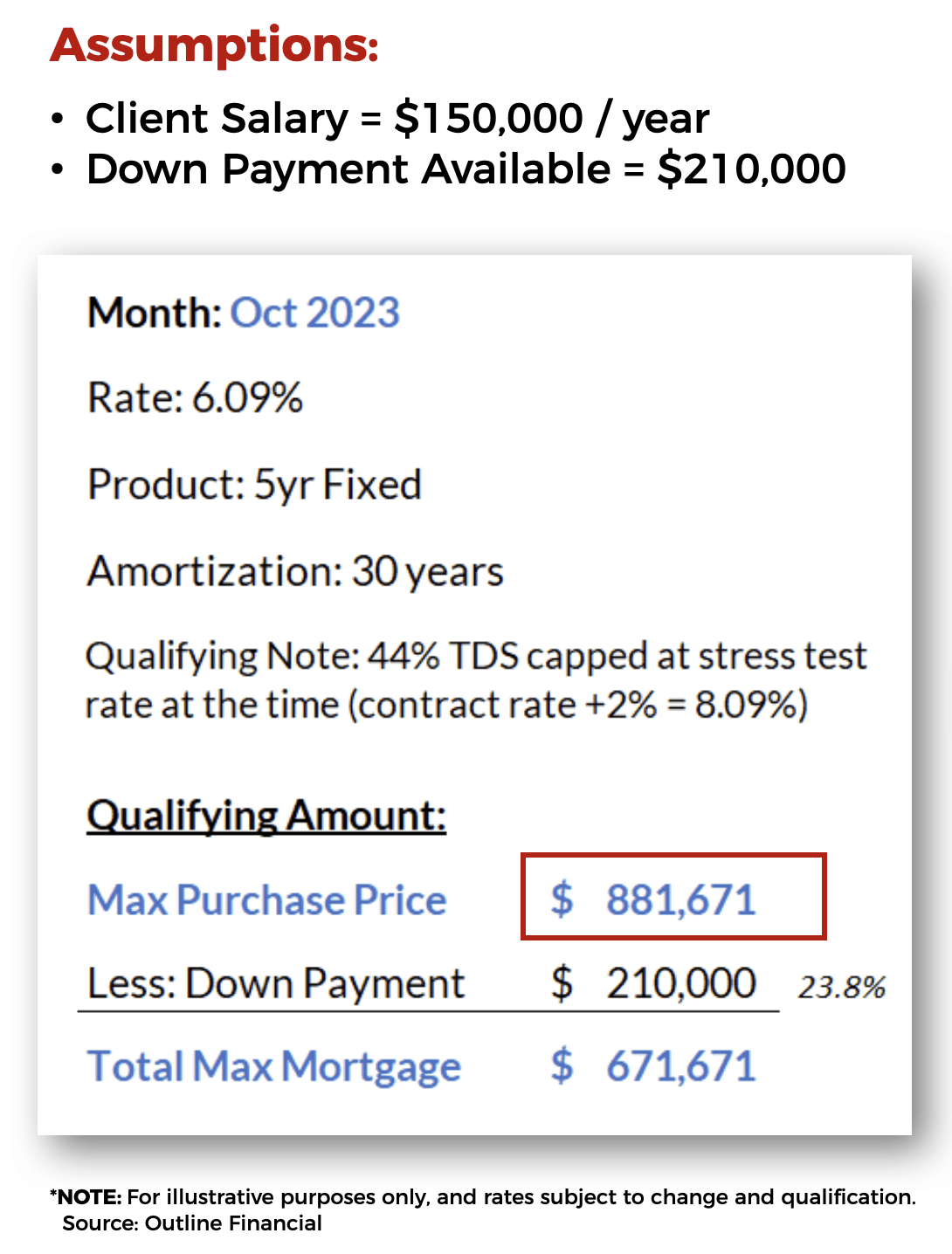

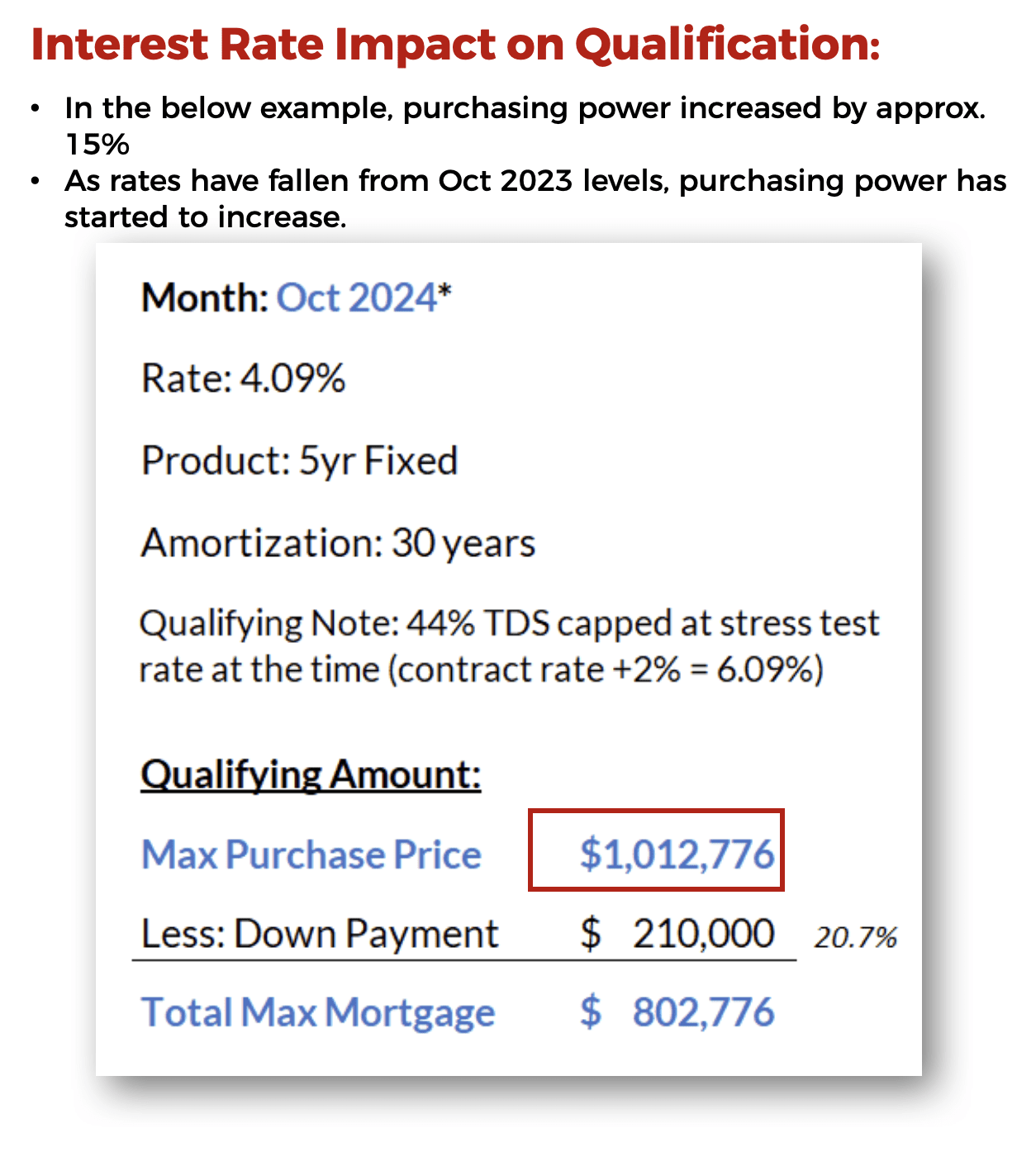

The massive impact of lower interest rates on monthly costs

Lower interest rates have had a dramatic effect on affordability.

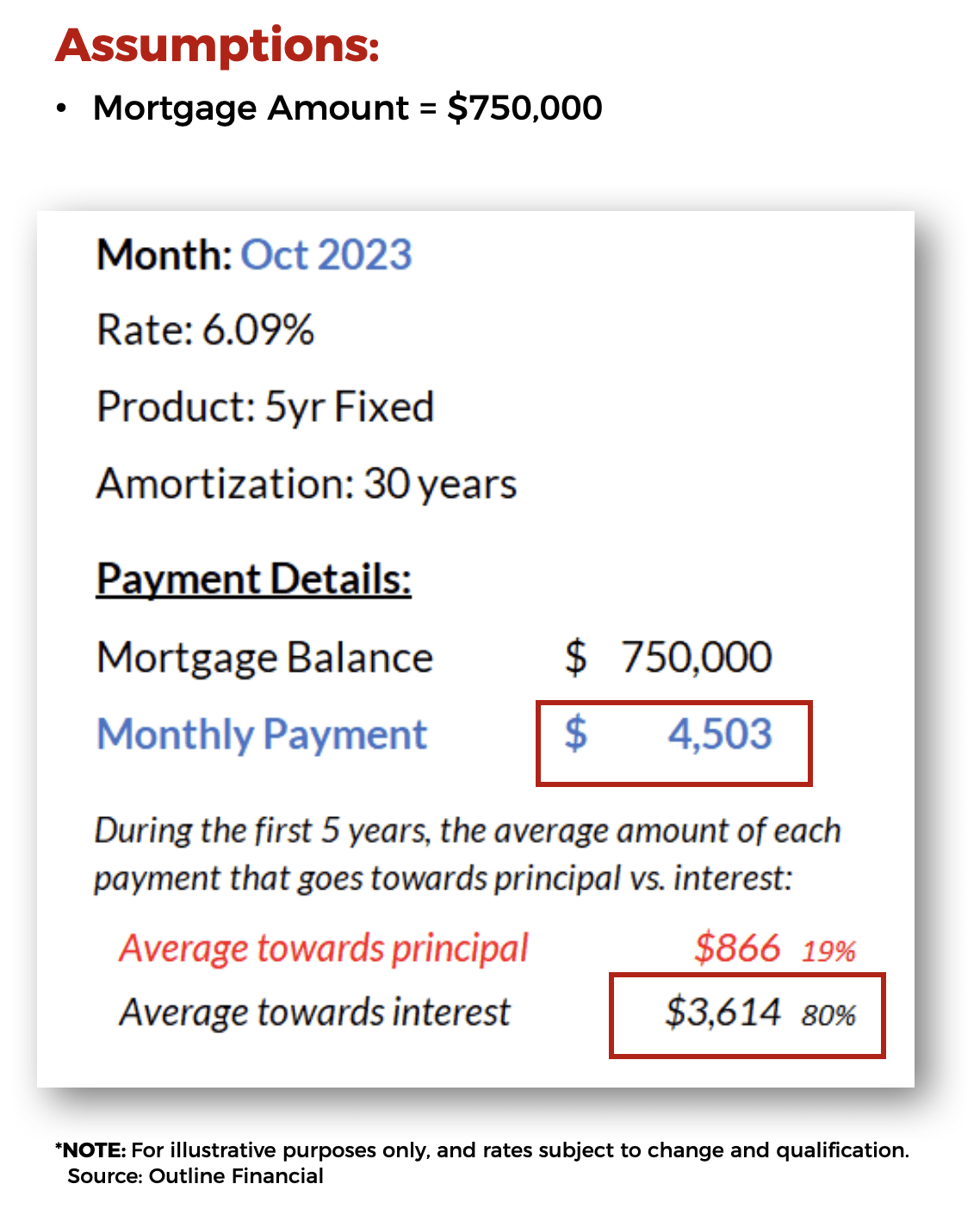

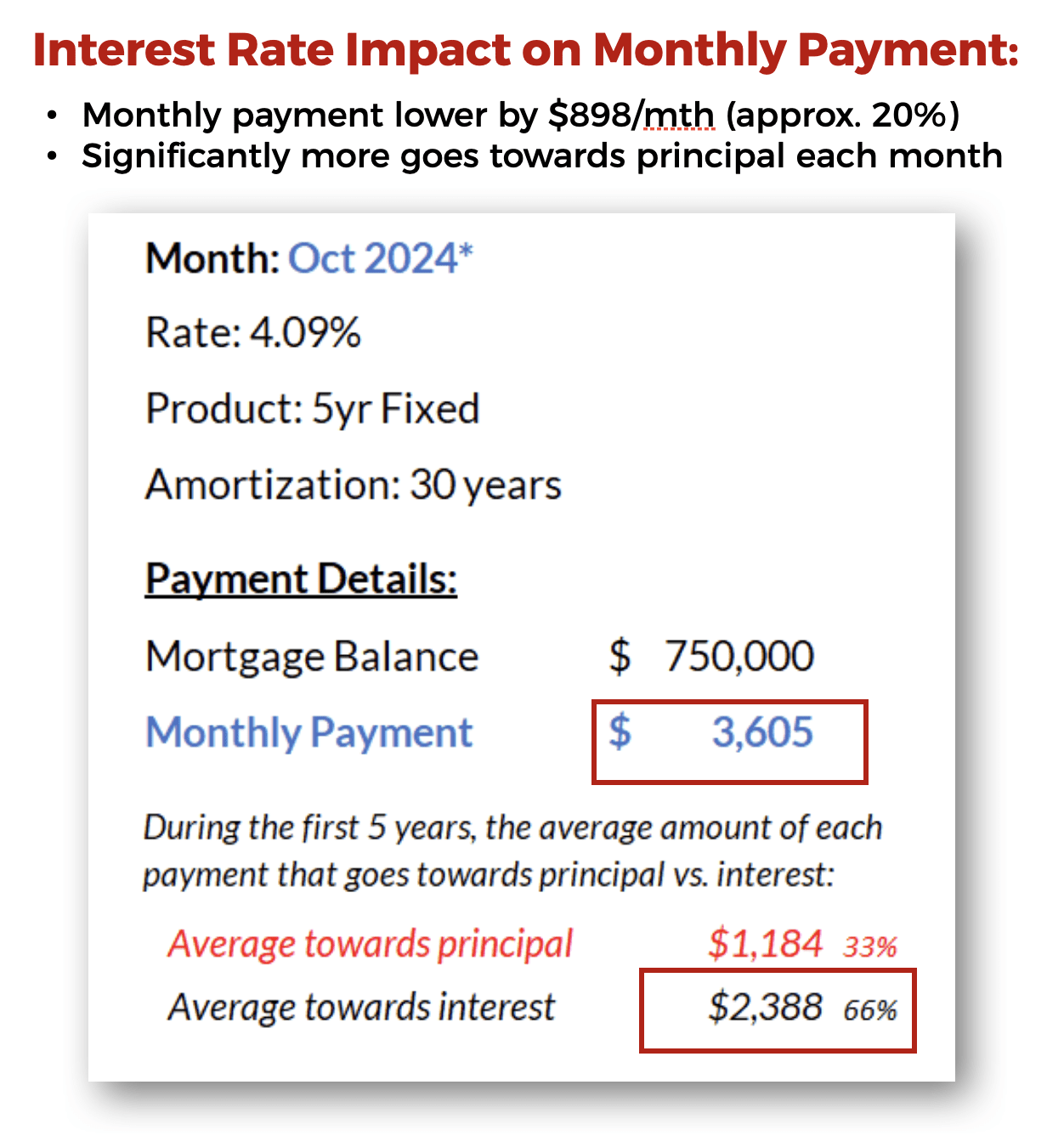

Consider a comparison of a fixed mortgage rate of 6.09% in October 2023 versus 4.09% in October 2024.

Using a Total Debt Servicing (TDS) ratio of 44%, a family’s purchasing power increased by approximately 15% with the lower rate.

TDS stands for “total debt servicing”, and it’s a measure of the debt from carrying the cost of mortgage, taxes, heat and condo fees (if any), plus any outstanding debt servicing from car payments, student loans, credit card interest, etc.

This is measured as a ratio against the gross family income.

For a $750,000 mortgage, monthly payments dropped by nearly 20%.

Not only are payments lower, but a greater portion now goes toward the principal.

These changes significantly enhance affordability and accessibility, and they’re expected to remain a driving force in 2025.

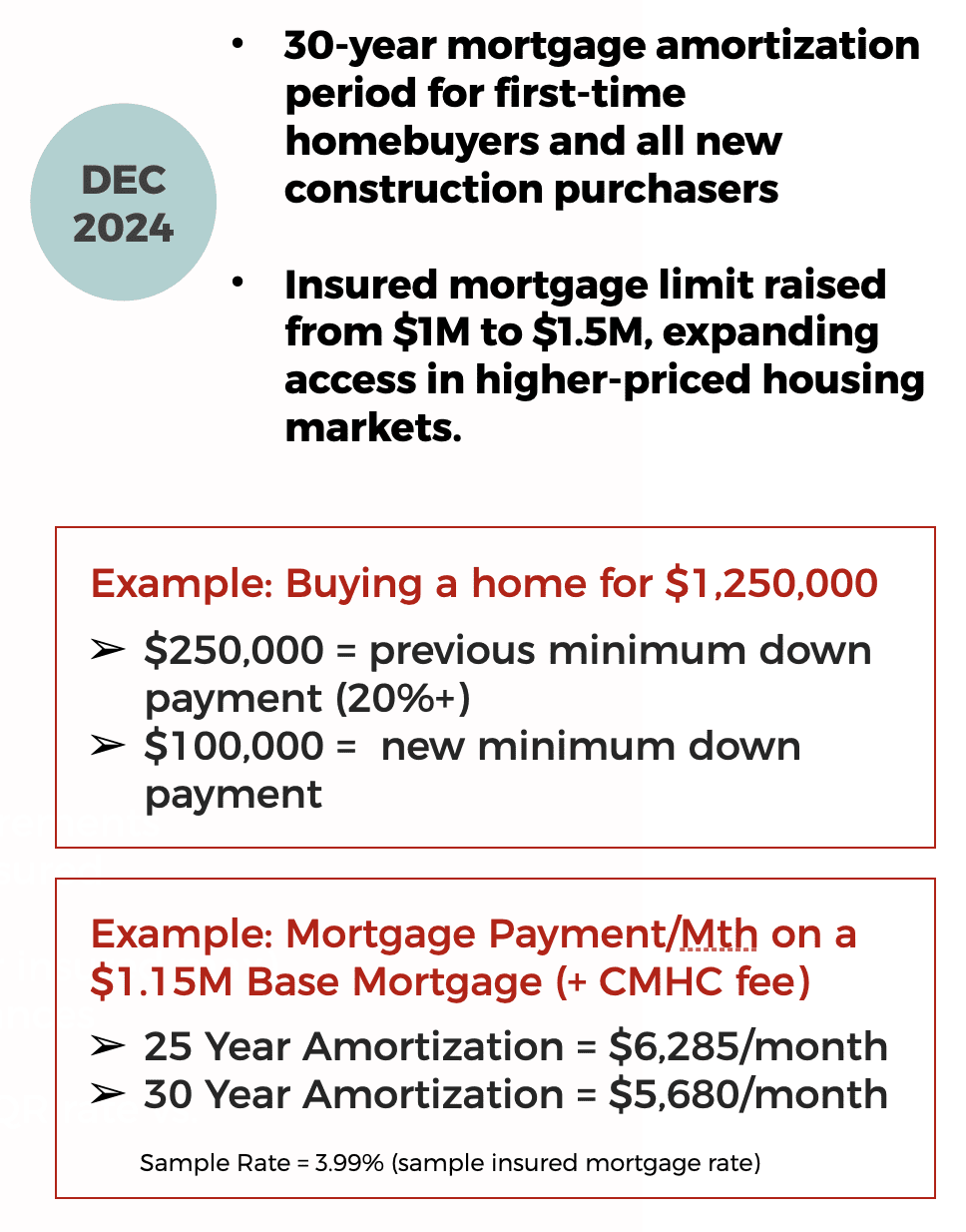

Changing mortgage rules

Lending policies have also evolved to support first-time buyers and those purchasing new construction homes.

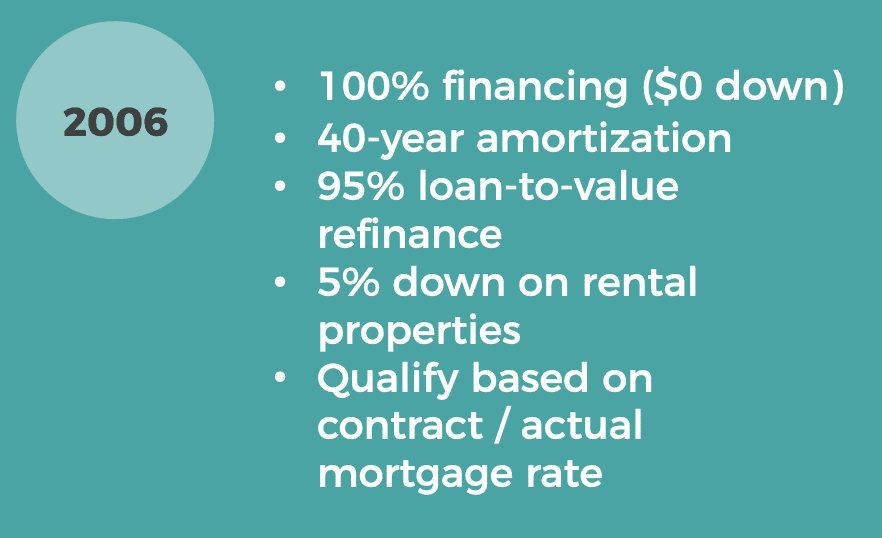

Back in 2006, it was quite easy to get a mortgage, with zero down financing and 40-year amortizations.

Looking back, we probably should have taken more advantage of this to invest in more real estate!

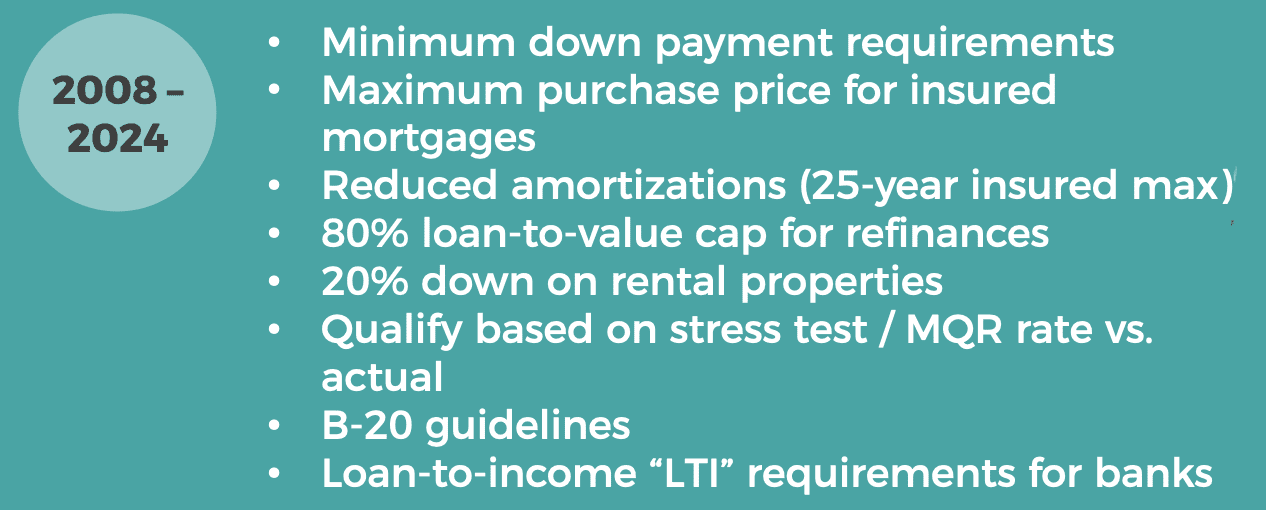

Stress tests and shorter amortization periods introduced post-2008 after markets collapsed made financing more challenging for buyers.

However, late 2024 brought new initiatives to lower minimum down payments for higher-priced homes above $1 million… and to extend amortization periods to 30 years for first-time buyers and all new construction buyers.

These changes are opening the door to homeownership for a broader audience. With these buyer-friendly policies, 2025 is shaping up to be a pivotal year for those entering the market.

Looking ahead & final thoughts…

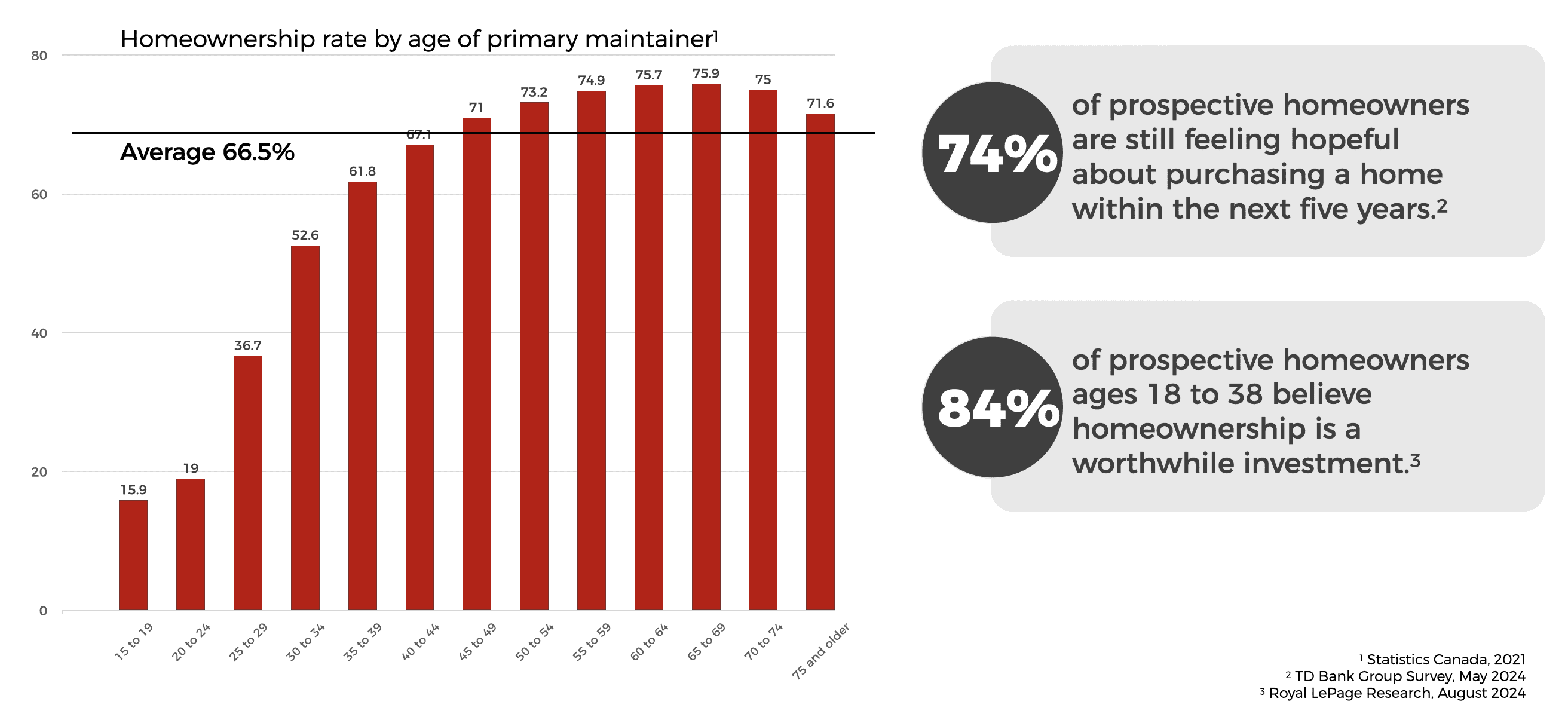

Based on surveys, Canadians’ desire to own a home remains strong.

As we’ve seen, several factors point toward a healthier real estate market in 2025.

Canadians are employed, have savings, and continue to prioritize homeownership.

Lower interest rates, favourable lending policies, and steady population growth are aligning to create a positive environment for buyers and sellers alike.

For Milton, the GTA, and the broader Canadian market, home price growth is expected to return to long-term norms, ending the era of market unpredictability.

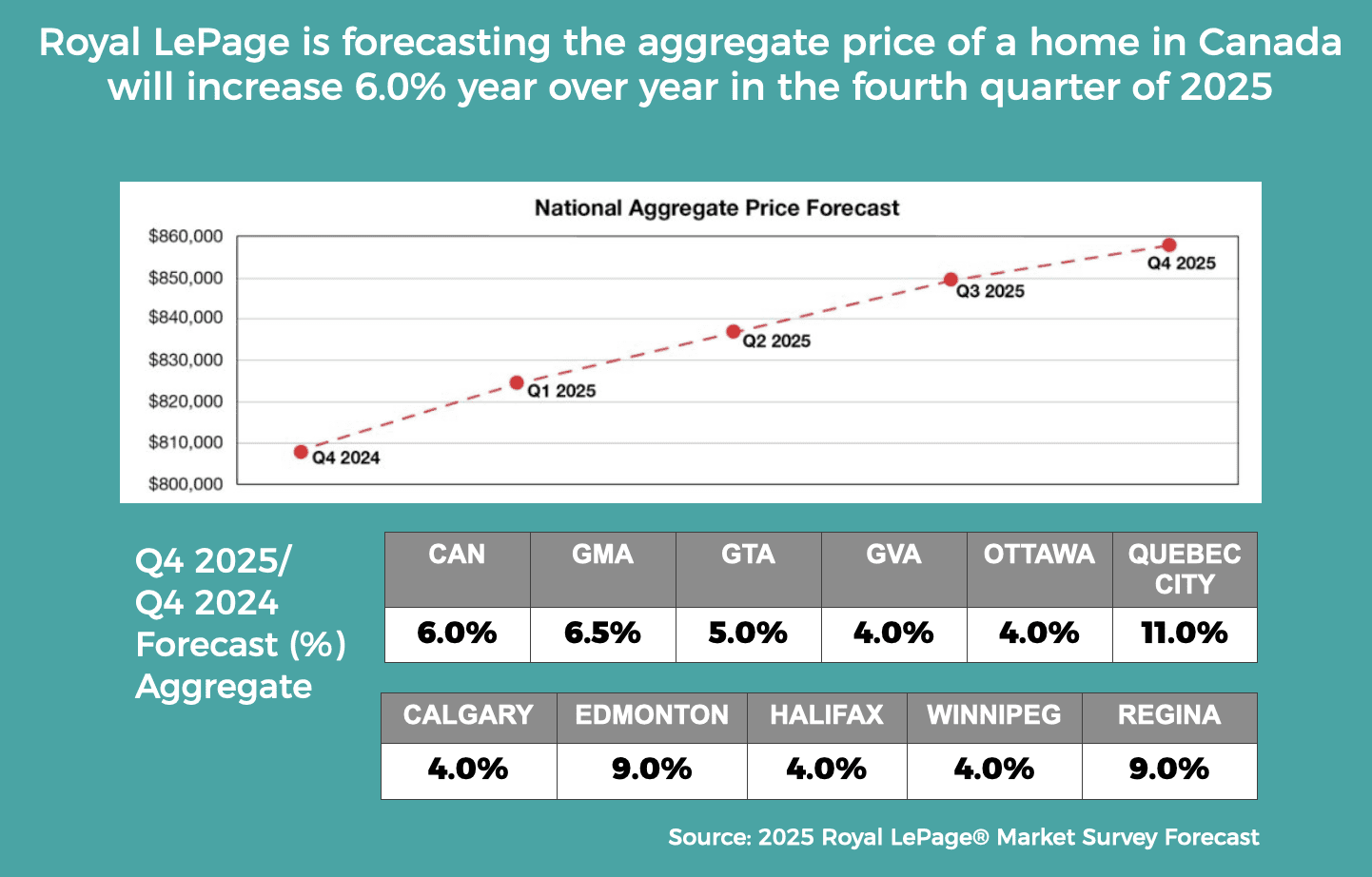

GMA = Greater Montreal Area, GTA = Greater Toronto Area, GVA = Greater Vancouver Area

Investors take note of the markets listed above. Watch Edmonton, Regina & Saskatoon and the major cities in Newfoundland in the next year or two. You’ve been warned!

Our prediction for the market

Drum roll please!

It’s time to make our prediction, based on everything you’ve read up to this point.

Historically, home prices have increased by just over 5% per year, and we expect the Canadian market to increase by 6% in the upcoming year.

It will be a relief for many to see a return of stability and normality in a market that has been in a state of turbulence for the last 4-5 years.

Finally, this is a question we have received by many readers… what about the trade wars mentioned by the incoming President?

We know that any tariffs imposed on Canadian goods will ultimately hurt Americans just as much, causing price increases, inflation, and making life LESS affordable for the citizens of the United States.

So… we are feeling optimistic that these were mostly empty threats.

However, any predictions are always written in pencil… not pen.

While uncertainties remain, the data strongly suggests that 2025 will bring stability and renewed confidence to the housing market.

Whether you’re planning to buy, sell, or invest, staying informed is key.

Reach out to our team to discuss how these trends can help you achieve your real estate goals in the year ahead.